What Is a Brokerage Account?

A brokerage account is like a savings account that you set up exclusively to invest, regardless of what investment option you choose.

You can use your brokerage account to buy stocks, bonds, mutual funds, index funds, exchange-traded funds, foreign currencies, futures, real estate investment trusts, precious metals, cryptocurrencies, and just about anything else that’s out there on the investment market.

Your brokerage account should work like a savings account in the sense that you can take money out of it anytime although it may mean selling some investments or having to pay capital gains taxes.

You can also set up an automatic transfer for it and some banks will let you link it to your checking account.

What Can You Do With a Brokerage Account?

When you open a brokerage account, you can use the account to gain access to different investment opportunities like stocks, mutual funds, bonds, EFTs, among many other types of securities. Besides, you can take part in trades that offer short-term benefits like trading in stocks.

You can invest in portfolios like gold that are long-term oriented. In addition, the account allows you to set aside some money for your retirement alongside other saving plans.

Savings Account Vs Brokerage Account

However, there’s one major difference between the two. Your savings account enjoys an insurance cover from the Federal Deposit Insurance Company up to $250,000 while your brokerage account has no insurance cover. So, if your investments fail, you can lose all the hard-earned money in your account in a snap.

The different brokerage accounts impose their own opening balance requirements. Some firms will ask for a minimum of $1,000, $2,000, or even more. Others would agree to a smaller amount when you open an account but will require you to deposit money every month automatically from your checking or savings account.

Once your account is ready, you can start buying and selling investments through it. The level of flexibility you can experience will depend on the firm that you choose to work with. And even if your account stays with a brokerage firm, you will own all the assets you will buy through the brokerage account.

What's the Difference Between a Brokerage Account and an IRA?

The main difference between a brokerage account and an IRA is the purpose for which you are opening an account. A brokerage account is an investment account that allows investors to buy and sell financial products such as stocks, bonds, and mutual funds. You can invest in both short-term and long-term investments, but you don’t get the tax incentives available in an IRA.

In this chart using FED Survey of Consumer Finances data, we can see that many people only start serious retirement planning after the age of 35. While under 35s have an average of $30,000 in retirement accounts, this increases significantly in the 35 to 44 age bracket. However, the increase is even more significant between the 45 to 54 age group and the 55 to 64 age group.

An IRA, on the other hand, is a tax-advantaged retirement savings account that allows investors to set aside part of their salary for retirement savings. The money grows tax deferred, meaning you won’t pay tax when you contribute to the account, but you will owe income taxes when you withdraw the money in retirement. Generally, IRAs are suitable for long-term goals.

| Classification | Brokerage Account | Retirement Account | Checking Account |

|---|---|---|---|

| Contribution limits | Does not restrict investment amount | Requires certain eligibility, and there are limits to how much you can contribute. | No restrictions on saving amount. |

| Taxes | Taxes are flexible | Taxation depends on the choice of your IRA | Does not attract taxes |

| Withdrawal charges | Flexible withdrawal depending on your needs. | Depending on your IRA account, you can incur penalties when you withdraw earlier than the maturity date | No access limit and withdrawals. |

| Purpose of the account | Goal is investment | Focuses in long term growth and retirement savings | Keeps your money safe |

| The fees | Does not attract maintenance and opening fees | Does not attract maintenance and opening fees | Can attract monthly maintenance fees |

Full-service Broker Vs Discount/Online Brokers

You can choose from several types of brokerage accounts.

The type that you should choose will depend on your investing goals, the kind of portfolio you want to build up and how much help from your broker you’d like in the selection and management of these investments.

Full-service Brokers

If you want a close professional connection with a financial advisor from your brokerage company, you should get a full-service brokerage account. The brokerage firm normally bundles with the account an opportunity to consult with in-house experts who can help you choose the instruments, conduct bigger-picture financial planning, look at some tax-saving strategies or just refocus your perspective when you become jittery because of sudden market deterioration.

Of course, it does not come cheap. Most brokerage firms will charge you expensive fees along the way, with some collecting big commissions while others will ask for a certain percentage of your assets on a defined schedule.

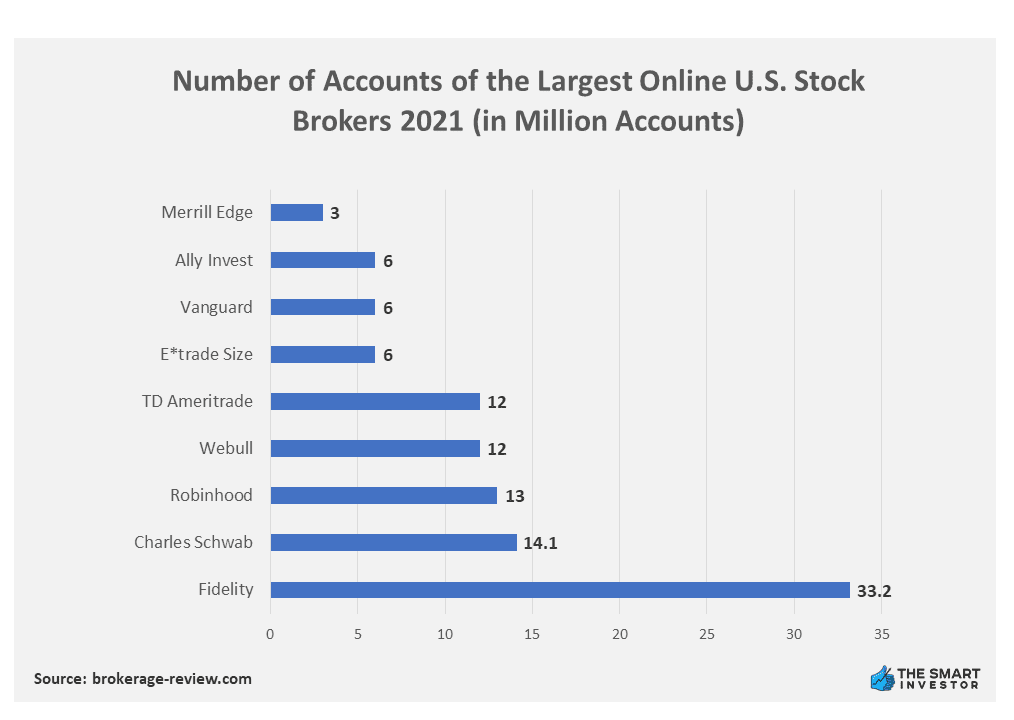

According to brokerage-review.com, Fidelity investment was leading with the largest brokerage accounts in the United States in 2021 at 32.2 million. TD Ameritrade, Webull, Robinhood, and Charles Schwab had over 10 million but less than 15 million accounts. Below 10 million brokerage accounts from the bottom up is Merrill Edge with 3 million, Ally Invest, Vanguard, and E*TRADE size, all tied with 6 million accounts.

Discount or Online Brokers

If you are comfortable with a self-service option, you can try an online discount brokerage account. They often charge the lowest fees because when it comes to choosing what investments to buy, they will leave you to decide for yourself.

You might find one or two that give access to advisors or investment research materials, but they won’t be as committed as the ones from your full-service brokerage. It’s a question of fees basically. Since you are not paying for the service, they won’t give you anything beyond your money’s worth.

Robo-advisors

If you have the full-service brokers on one end and the discount/online brokers on the other end, you’ll find the Robo-advisors in the middle. A Robo-advisor is an automated platform that can provide you with financial planning services (such as building your investment portfolio) but without the services of a human advisor.

Similar to full-service brokers, the best Robo-advisors will choose investments for you and conduct trades on your behalf. Since they rely on an algorithm, they can’t fully customize a portfolio to exactly to your requirements.