Table Of Content

With the rate of inflation on the rise, many people are looking for ways to invest and manage money during inflation.

Traditionally high yield savings and gold have provided safe avenues of investment, but which one is better in high inflation?

Are Gold and High Yield Savings Accounts Considered Inflation Hedges?

High Yield savings accounts have traditionally been a go-to for those looking for an inflation hedge. While they may not offer the returns that you may be able to achieve with other investments, they are safe and provide great liquidity.

As the FED adjusts the interest rates to combat increasing inflation, the higher interest rates are passed on to deposit customers. This means that you can access higher rates of interest, while still being able to access your money.

Although a high-yield savings account may not completely offset the higher rates of inflation, they do provide an opportunity to move funds if the interest rates become particularly unfavorable.

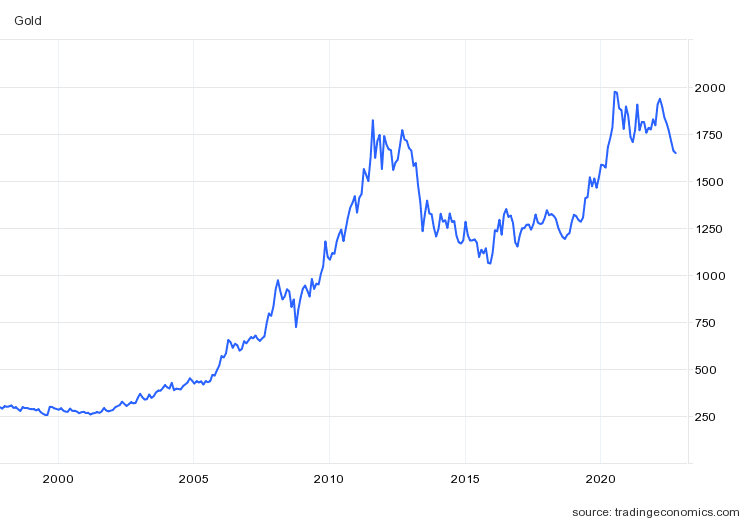

Gold has also been considered an inflation hedge, as it tends to be far less volatile compared to many other securities. Gold tends to be relatively stable, so while you may not enjoy massive returns, it does provide a place to store your money with little or no value loss and minimal risk.

High Yield Savings Accounts: What To Know?

A high-yield savings account works in a very similar way to a regular savings account, but in return for a higher interest rate, there are typically restrictions in place.

For example, you may have to make a minimum deposit and agree to a maximum number of withdrawals. If you exceed the number of permitted withdrawals, you are likely to incur an interest penalty or have your account converted to a regular savings account.

Of course, there are both positives and potential negatives associated with high-yield savings accounts, which can help you to determine if they are the right choice for you.

Pros & Cons of High Yield Savings Accounts

Pros | Cons |

|---|---|

High Rates | Variable Rates |

Daily Compound Interest | Interest Penalties |

FDIC Insurance | Transfer Delays |

Liquidity |

- High Rates

The best high-yield savings accounts currently offer +4% APY. This is high interest on deposit, especially considering the low interest on deposit you could get in the last 15 years.

- Daily Compound Interest

Typically high-yield savings accounts compound the interest daily, which means that you can grow your account balance a little quicker compared to the traditional monthly compound interest savings account.

For example, with daily compound interest, you can save $1,000 in a year by simply making a $20 deposit each week.

- FDIC Insurance

High yield savings accounts are typically FDIC insured, which provides up to $250,000 of coverage should the financial institution fail.

- Liquidity

Although there may be interest penalties, you can access your funds at any time if you have a financial emergency.

Additionally, it is easy to transfer your funds to your other bank accounts.

- Variable Rates

The interest rates on these accounts are typically variable, which means that they can fluctuate.

So, while you may open an account when rates are high, this will not last forever.

- Interest Penalties

As we touched on earlier, if you exceed a specified number of withdrawals per month, you’ll incur an interest penalty.

- Transfer Delays

While you can move funds from one bank to another one, you may have some transfer delays of up to 48 hours.

How Does Gold Investing Work?

Gold is a physical, tangible asset that typically will hold its value. But, gold will not pay yields and the value does not greatly fluctuate. This means that you can use it to store your funds, but it is not a growth asset.

Traditionally, you could purchase physical gold, but many of us don’t have the facilities to store an abundance of this precious metal. Fortunately, there are several ways that you can invest in gold without needing to physically hold on to the gold yourself.

You can either buy gold shares or ETFs or purchase gold with a dealer that offers holding facilities.

Pros & Cons of Gold Investing

Pros | Cons |

|---|---|

Stability | No Yield |

Tangible Asset | Lack of Liquidity |

Simple |

- Stability

Gold tends to be relatively stable with little price volatility, regardless of the interest rate changes in the economy.

This makes it a good place to store funds if profits and growth are not a big priority for you.

- Tangible Asset

Many people enjoy the reassurance of having a tangible, physical asset.

If you prefer you can buy popular gold coins such as the American Eagle or the South African Krugerrand, or purchase other forms of gold that you can store yourself, meaning you have a tangible asset on hand.

- Simple

Gold has been a currency in various areas of the world for centuries, which means that it is a simple form of investing.

- No Yield

While there can be short term volatility, you cannot expect to make a real profit from gold holdings.

- Lack of Liquidity

Unless you invest in physical gold, if you purchase gold mining stocks or ETFs and want to release the funds, you can’t simply take it to your local bank and cash out.

If you are in a hurry to liquidate funds, you may even take a loss when you sell your gold.

Gold vs High Yield Savings: Key Things to Consider

If you’re considering gold or high yield savings accounts but are not sure which is best for you, there are some key things that you need to consider.

- Liquidity: Liquidity is a major consideration for any investment and it is important to consider whether you anticipate needing access to your funds in the near future. If you have a financial emergency or a more profitable opportunity arises, can you release the funds as you need them? In the case of a high yield savings account, the answer is yes, but gold can be far trickier.

- Returns: If you are interested in getting a return on your investment, you’ll need to look to high-yield savings accounts, but if your priority is simply holding your money in an inflation hedge

- Ease of Access: Many high street and online banks offer high-yield savings accounts, but if you want to invest in gold, it is a little trickier. You’ll need to use a gold brokerage or find a gold holding company if you don’t want to store your own gold.

When to Consider Gold Investing Over High Yield Savings

It makes sense to choose gold investing if you’re looking for a potential hedge against inflation and challenging economic conditions. Gold is typically positively correlated to difficult economic conditions.

This means that gold is likely to go up during shaky economic conditions, providing a helpful option if you want to try to plan ahead.

Gold can also provide an opportunity for diversification. Rather than tying up all of your money in one asset class, investing in gold can help you to build a diverse portfolio to manage risk and return. With the right allocation, gold can be a good choice for a balanced portfolio, depending on your volatility tolerance, liquidity needs and time horizon.

While gold can have some short-term volatility, if you are anticipating a longer period of uncertainty and want to hedge against inflation, it makes sense to choose gold investing. Although you can’t expect massive returns, gold investing can provide a safe place to park some funds.

When to Consider High Yield Savings Over Gold Investing

If you have a more short term approach, a high-yield savings account provides a better option. You can enjoy decent liquidity, as you can access the funds at any time. Although there may be an interest penalty if you have exceeded the number of permitted withdrawals in a calendar month, if you have a financial emergency, you can quickly get your hands on your cash.

It also makes sense to put your money in a high yield savings account if you may have other opportunities on the horizon. If you simply want a place to store some funds while you’re awaiting an investment option or you could have an investment opportunity, you can access the funds with little or no penalty.

High yield savings accounts are also a good option if you are looking to generate returns. While they may not be completely inflation busting, the higher rates can allow you to retain the buying power of your money.

Bank/Institution | Savings APY |

|---|---|

American Express | 3.30% |

Capital One | 3.30% |

Upgrade | 3.05% |

Marcus | 3.65% |

Discover Bank |

3.30%

|

Lending Club | 4.00% |

Quontic | 3.50% |

UFB Direct | up to 3.9%

|

Alliant Credit Union | 3.06% – 3.10% |

Ally Bank | 3.20% |

SoFi | up to 3.80% |

How FED Interest Rate Hikes Impact Gold Investing and Savings Accounts

Gold prices are not a function of interest rates. As a commodity, gold is impacted by supply and demand rather than interest rates. The price of gold increases when there is a stronger demand, while a supply surge can cause the price to drop.

However, the level of gold supplies tends to change very slowly, as it can take 10 years plus for discovered gold deposits to convert into producing mines.

So, FED interest rate hikes will not directly impact gold prices, but there could be an impact due to economic conditions.

As rates increase in response to high inflation, many investors may switch to inflation hedge products like gold, increasing the demand. If the demand starts to outstrip supply, the price of gold will go up.

On the other hand, FED interest rate hikes have a direct impact on high yield savings accounts. These types of accounts typically have a variable rate, which means that the FED increased rate will be passed on to customers via higher savings account rates.

So, the funds in your high yield savings account will attract a higher interest return, but if inflation remains high, it may not be able to compensate for the reduced buying power of your funds.

FAQs

How to open a high yield savings account?

Opening a high yield savings account is very similar to opening a standard savings account. If you already hold an account with a bank or financial institution, it is remarkably easy.

However, if you’re new to the bank, you’ll need to complete an application form online or visit a local branch.?

Can I open a high yield savings account online?

Yes, many banks offer the facility to open a high yield savings account online. In fact, many banks exclusively offer high yield savings accounts online.

What are the best savings account rates?

High-yield savings accounts typically offer multiple times the standard savings rates.

For example, Marcus’ high-yield savings account offers a rate of 3.65%, which is four times the average savings rate.

How to find a gold dealer?

If you're looking to buy physical gold, there are many online gold dealers you can buy from. Make sure your dealer is reliable, ask questions and read reviews before ordering.