Table Of Content

In times of financial uncertainty, one of the best alternatives for riskier investments such as stocks or real estate is the US treasury bonds.

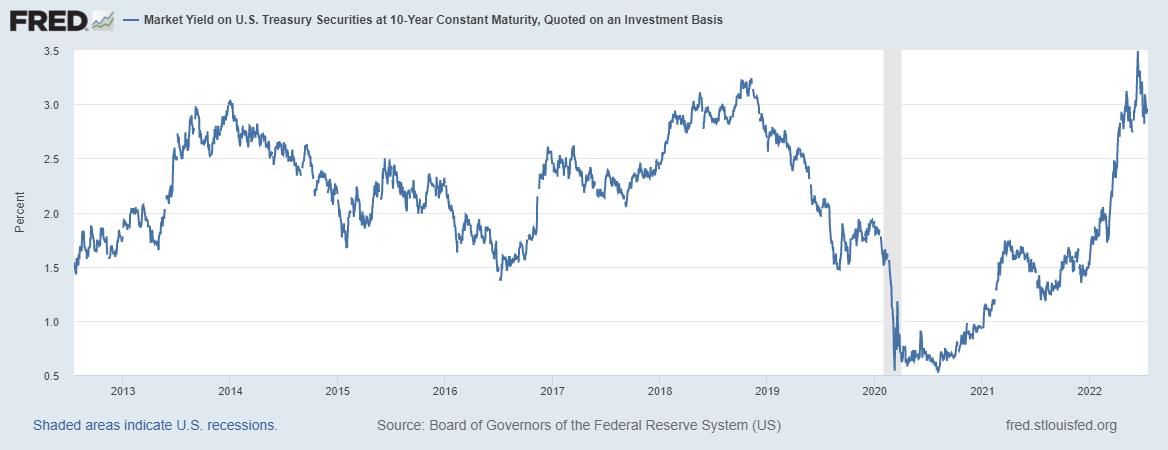

The high inflation during the last year is drastically affecting US treasury bonds yield, and investors can get more than 3% interest on US 10 years bonds.

Key Takeaways

- One of the main advantages of investing in US treasury securities is the fact that interest received from them is exempt from federal and state income tax. This can be especially appealing for those investors who are in higher tax brackets.

- Another advantage of investing in US Treasuries is that it is a very liquid investment. If an investor needs some cash, he or she can liquidate US treasury bonds without any complications or significant delays.

- While Treasury Inflation-Protected Securities do offer investors some hedge against inflation, treasuries with fixed interest payments are still exposed to inflation risk.

What Are US Treasury Bonds?

Technically, U.S. Treasury bonds are certificates of indebtedness emanating from the U.S. federal government. This actually means that each time you buy a Treasury security, you are in effect, lending money to the government for a pre-determined period of time.

They are available in different forms namely: Treasury Bills, Treasury Notes, Treasury Bonds, Floating Rate Notes (FRNs), and Treasury Inflation Protected Securities (TIPS). The generic term for all these is “Treasuries”.

Were we to name the one differentiator between bills, notes, and bonds, we would have to say it’s the length until their maturity date. See for yourself:

- Treasury bills have less than one year to mature

- Treasury notes have terms of 2, 3, 5, and 10 years

- Treasury bonds take 30 years to mature

- Treasury Inflation-Protected Securities (TIPS) have 5, 10, and 30-year maturities

- U.S. Savings Bonds have varied maturity dates but they generally stop earning after 30 years

- Separate Trading of Registered Interest and Principal Securities (STRIPS) ride on the original instrument’s maturity date

- Floating Rate Notes usually carry a 2-year maturity

Here's a summary of the main pros & cons :

| Pros | Cons |

|---|---|

| High Credit Quality | Low Yield |

| Tax Advantages | Call Risk |

| Liquidity | Interest Rate Risk |

| Choices | Credit or Default Risk |

| Friend Until Retirement | Inflation Risk |

| Restrictions and Penalties |

Treasury Bonds Advantages

Any investment has its own pros and cons and no single instrument is absolutely perfect. The same thing applies to Treasuries. Therefore, you should understand its advantages (and disadvantages) before you say that it is the right option to achieve your financial goals.

Treasury securities do not burden investors in paying maintenance fees – that’s just one advantage. Here are some more of them:

- High Credit Quality

Obviously, no private debt instrument issuer would ever beat the U.S. government in the area of creditworthiness. Needless to say, Treasury securities have the highest credit quality among the instruments in the U.S. market if not in the world.

Just imagine the taxing power of the most powerful government in the globe and size of the U.S. economy that secure these instruments. But do take note that in August 2011, Standard & Poor downgraded the long-term sovereign credit rating of the USA to AA+ from AAA.

This was amidst concerns about the U.S. budget deficit and the direction of the U.S. economy. The credit-rating agencies have since upgraded this rating.

- Tax Advantages

Here’s something that’s really interesting for investors: you won’t have to pay state and local income taxes on interest income from Treasury bonds. However, you still have to pay federal income taxes as you would from your income in a majority of investment options.

And you have to remember that when you sell your bond or redeem it at maturity, some components may then become taxable. Purchasing a bond at a market discount on the secondary market is different than buying a bond at Original Issue Discount (OID) from the point of view of taxation.

For example, if you buy the bond at a discount (the purchase price is less than the face value) and you hold it until maturity or sell it at a profit, that gain will be taxable. You have to pay federal and state capital gains taxes on them. However, if you buy it at OID and you hold it until maturity or sell it at a profit, your gains will fall into a different type of income.

- Liquidity

If you were to dig deep into the volume of Treasuries that investors buy and sell throughout each trading day, you will likely become awestruck by the amount involved. Not only do individual investors chug them up but more so do big financial institutions, corporate investors, and even foreign governments in many cases. You don’t have to be a financial wizard to conclude that liquidity is probably the last thing to worry about.

If you want to buy Treasury securities such as bonds, there are two venues where you can go. The most common is through the secondary market which enjoys the distinction of being the most actively-traded market. Or, you can participate in regularly scheduled auctions for them; just check out the Auction Schedule.

In the secondary market, you can find postings for Treasury bills, notes, and bonds with active bids and offers. Another important thing to remember is that in this arena, you’ll find that the spreads (the difference between bids and offers) are the narrowest in the bond market. Watch out for the few times when US treasury bonds reach their highest volatility.

For example, when the government releases significant economic data to the public, it normally affects US treasury bonds.

- Many Choices

As we’ve said, Treasuries come in various maturities – from 2 to 30 years. Here’s the thing about securities: the longer maturities would always offer higher coupons.

One more thing you should note is that Treasuries come in different structures. There are Treasuries with coupons, zero-coupons, and TIPS, whose principal and returns move up and down to reflect changes in the consumer price index.

So, as an investor, you would not find yourself contained in a box but rather one who can rummage through a box to find the best product for your needs.

- Your Friend Until Retirement

If the purpose of investing is to build a retirement nest egg, Treasuries are great. They’re obviously safer than stocks so that eliminates some tensions and fear for the future.

Not only that, the interest payments that you will receive can help you create an alternate income stream when you retire.

Top Offers From Our Partners

![]()

![]()

![]()

Disadvantages Of Treasury Bonds

Treasuries do make a safe investment but like any other instrument, they have some handicaps. For investors who are looking for a quick return, this falls way below that expectation.

Here are some more disadvantages:

- Inflation Risk

Inflation risk is what happens when the value of your investment declines because of the increase in the inflation rate. Although this risk is real for practically all investment instruments, it’s a much bigger reality for Treasury instruments since they generally have lower rates.

For example, if your Treasury bond has an interest of 2.84% and the inflation rate reaches 3.5% or rises by just 1%, your investment is losing. Technically, the real value or purchasing power of your investment and earnings has declined.

There’s no question though that come maturity date, you’ll get the principal back. However, it will be worth a lot less in terms of monetary value.

Of course, there’s a way to lessen this problem and that is through TIPS or Treasury Inflation-protected Securities which adapts to the current inflation rate. Or you may invest in mutual funds that also invest heavily in TIPS.

- Low Yield

Yes, they give you peace of mind but don’t expect it to be like winning the lottery. The rates of returns are different for each type of instrument but they’re basically similar when it comes to overall returns.

Even if you hold them until maturity to cash out, the proceeds will typically be low. Other investments that carry bigger risks than Treasury bonds offer greater returns – that’s how things work in the financial investment world.

So, if you’re adventurous when it comes to your money or very keen on getting higher returns on your investments, Treasury securities would sit at the bottom of your priority list, and you'd probably need to consider corporate bonds instead. And if you’re in a hurry to cash out, Treasury bonds will take you at least 10 years before you can redeem them.

- Interest Rate Risk

Treasuries are not immune to interest rate risk – the fluctuations in interest rates affect them. What’s more, the degree of volatility increases as the instrument nears its maturity. When interest rates go up, the prices normally go down.

- Call Risk

Some treasury securities have call provisions that allow the government to retire them before the originally-stated maturity date. The government does this during times when rates fall.

- Credit or Default Risk

All investors need to know that all bonds carry the risk of default (where the issuer cannot pay the interest or principal on time). The U.S. Government remains to be the strongest government in the world but there were times that it shut down for a period of days.

If you are a serious investor, you should monitor current financial and political events and pay attention to national debt issues, GNP, Treasury yields, falling of the U.S. dollar and other signs that may indicate a default risk is imminent.

- Restrictions and Penalties

If you redeem US treasury bonds before their maturity date, you might incur some penalties. At best, some restrictions may limit what you can or can’t do at certain times.

How Do You Purchase Treasury Bonds in the United States?

You have three options for purchasing US treasury bonds. A non-competitive bid auction is the first option. This is for a buyer who is serious about the note and is willing to accept any yield. Individuals most commonly use this strategy. To complete their purchase, consumers simply need to go online. This approach allows a person to purchase up to $5 million in Treasuries.

A competitive bidding auction is the second option. Some investors will only buy a Treasury if they can achieve the yield they want. It's for them that we've devised this strategy. They must, however, proceed through a bank or a broker. This approach allows an investor to purchase up to 35 percent of the Treasury Department's first offering amount if they have the necessary cash.

Buying them on the secondary market is the third option. The trading system where Treasury owners sell their assets before they mature is known as the secondary market. To make transactions easier, banks or brokers function as middlemen.

If an investor does not wish to invest directly in individual Treasuries, he can invest in a Treasuries-focused mutual fund or exchange-traded fund (ETF). Apart from Treasuries, some funds own other fixed-income assets or derivatives, so investors must be aware of the investment mix as well as any fees or other expenses.

Banks and traders do not trade savings bonds, unlike the other marketable US Treasury securities mentioned in this guide. A savings bond owner cannot resell or distribute his or her bond to another person. When buying a U.S. savings bond as a gift, you must first register the receiver, who will be the bond's sole owner. As a result, it won't count towards the buyer's annual purchase limit.

Savings bonds are one of the safest investments, but over time investors have become a little more confident about taking on riskier investments, as you can see from this chart using FED Survey of Consumer Finances data

Which U.S. Government Bonds is Best For Inflation Hedging?

Treasury inflation-protected securities (TIPS) are a simple and effective approach to avoid inflation risk while receiving a guaranteed real rate of return from the US government. TIPS modify their price to maintain their real value as inflation rises. TIPS have one disadvantage: they often pay lower interest rates than other government or corporate securities, making them unsuitable for income investors. Their principal benefit is inflation protection, although their utility falls when inflation is low or nonexistent.

If inflation has increased the value of the principal, the investor would receive the higher, adjusted amount back. However, in a case when inflation has decreased the value, the investor will receive the original face amount of the security.

Let’s look at an example of how inflation-indexed securities work. Please note that this simplified example is for illustration only and does not necessarily reflect current market conditions.

- At the beginning of January, you invest $2,000 in a new 10-year inflation-indexed note. The note states a 3% annualized interest and it is payable semi-annually.

- In the middle of the year, the CPI indicates an inflation rate of 2% for the first six months. What happens then is that they will adjust your principal upward to $2,040 ($2,000 x 102%) and your resulting interest payment would be $30.60 ($2,040 x 3.0% x 6/12) for the interest earned for the first 6 months.

- At year-end, the index indicates that inflation has risen to 3%. This will bring the value of your principal to $2,060. Under this amount, your second interest payment would be $30.90 ($2,060 x 3.0% x 6/12).

FAQs

Can I lose money when investing in treasuries?

Since the U.S. government guarantees its payment, as long as the US government doesn't go bankrupt, it is unlikely that you will lose money in government bonds. In contrast to corporate bonds, however, government bonds have lower interest rates. You must keep a government bond until it matures in order to enjoy all of its benefits.

You risk losing money if you sell the government bond before it matures. This indicates that the issuer will only guarantee your principal if you wait until maturity. However, you should be aware that inflation and interest rate changes have a significant impact on the interest rates of government bonds.

How are Treasury securities with inflation protection (TIPS) taxed?

In general, TIPS interest income is taxed at the same federal income tax rates as any other nominal Treasury security. They also attract Phantom Income taxation, which is the tax levied against the growth in value of the premium during inflation.

However, by employing deflation adjustments to balance it, you can lessen the effect of this fee. Typically, deflation causes your principal value to decrease. The alternate strategy is to purchase your TIPs using a tax-deferred account, but you should speak with a tax professional to see whether this is a wise course of action.

What distinguishes treasury securities from corporate bonds?

The issuer makes a clear distinction between the two. The federal government, acting through The Bureau of the Fiscal Service, is the issuer of treasury securities. In contrast, the corporate bond issuers are various private organizations with various credit ratings to denote their legitimacy.

The most reliable kind of bonds in terms of trustworthiness are U.S. Treasury securities. They do, however, provide cheap interest rates. Corporate bonds, in contrast, offer greater interest rates but may also be riskier, depending on the issuer's credit standing.

Where can I sell my Treasury bonds?

Your broker's platform will determine how you sell your Treasury bond. You must first double-check the market's current problem. Next, decide who will act as your sales intermediary.

To find a willing buyer on your behalf, you can either use your broker, an online dealer, or a business bank. Keep in mind that T-bonds are not subject to penalties even if you sell them before they mature. However, you must remember you can always suffer some charges.

What kind of bond should I buy?

You must compare each bond's prospective rewards to its associated risks when determining which bond is the best one to invest in. Treasury bonds are among the best bond types to invest in if you're seeking for a safe bond with a guaranteed return. These bonds, however, have a modest interest yield and are quite susceptible to inflation.

Corporate bonds are the greatest when contemplating increased interest rates, but they come with significant dangers. The amount of interest, nevertheless, will depend on your credit rating. The risk and interest rating are both lower the higher the score. Corporate bonds with weaker credit ratings, on the other hand, have higher interest rates but higher risk.

Does the Risk versus return for Treasury bonds worth it?

You should be aware that risks have an impact on a treasury bond's return while investing in treasury bonds. Treasury bonds contain some risks, while being among the safest bonds on the market.

Inflation and interest rate risk are the two main dangers that government bonds encounter. The bond's interest rates are impacted by inflation.

For instance, if the bond's interest rate is 4 percent but inflation increases by 2 percent, the bond's interest rate will now be 2 percent. In contrast, the underlying intrinsic value of the issued bond is impacted by the interest rate risk. Its value decreases when the interest rate rises and vice versa is true.