Table Of Content

If there is a threat of recession, one of the first things many people worry about is the impact on the real estate market. While a recession can be tough on the labor market, it also makes it difficult for people to purchase their first home or move to a new home.

In fact, there is a knock on effect across the whole economy. But, how does falling real estate prices impact the banks? Here we’ll explore what happens to big banks if real estate prices were to drop by 25%.

Real Estate Market Troubles

While the economy seems to be in a little turmoil at the moment, currently, the real estate market is actually showing some positive signs. According to the National Association of Realtors, the inventory of properties on the market is low compared to historical standards, but it is up slightly from last year. This means that there are multiple bids for the same property, which makes it a sellers market.

However, this lack of inventory may stem from the uncertainty within the economy. With interest rates on the rise and high rates of inflation, many homeowners may be reluctant to consider upgrading, which will lead to fewer transactions in the real estate market.

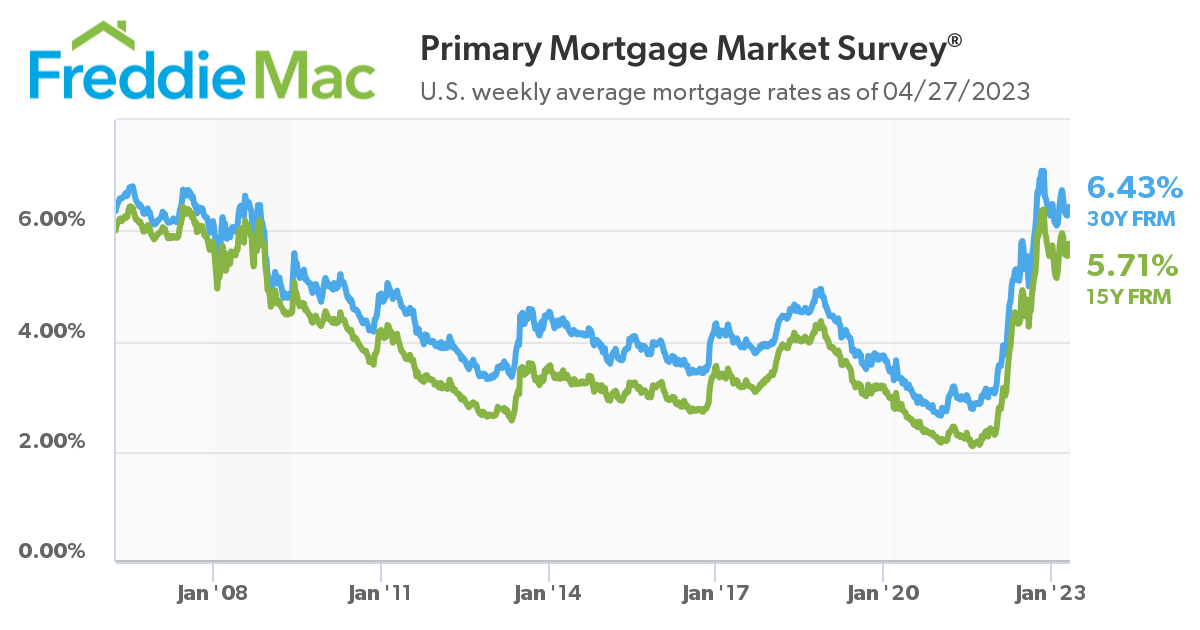

In fact, since the FED has increased the base rate seven times so far in 2023, as of April 2023, mortgage costs have significantly risen. Mortgage rates rose throughout 2022 and 2023 started with mortgage rates twice as high as at the start of 2022.

In a Bankrate analysis, the cost of the median home represented 19% of the median household income. This has increased to 24% in 2023. This represents thousands of additional dollars needed for mortgage costs each year. So, homeowners who are already feeling the pinch of the rising household costs are unlikely to consider upgrading their home.

Why Banks Should Be Worried

Although you may have some appreciation for how the real estate price drops may impact, there are a number of reasons why banks should also be worried. These include:

- Less Business: The main reasons why banks should be concerned if real estate prices drop is that it will generate less business. There will be fewer customers looking at obtaining a mortgage and those that do may be looking for lower sums.

- Higher Default Risk: When economic times are tough and real estate prices drop, it can lead to a scenario where homeowners end up with negative equity and cannot sell to cover debts. If a homeowner is struggling financially, but selling their home is not feasible, it increases the risk that they may default on their financial obligations.

- Greater Losses: Banks operate on a balance of attracting depositors and using those funds to offer financing for mortgages and loans. Unfortunately, when real estate prices drop and there is market uncertainty, not only are there more potential losses from mortgage customers, but depositors may consider putting their money into more inflation proof investments. This can put the bank at risk of financial instability.

- Exposure to Commercial Real Estate: Unfortunately, the issue of the real estate market is not restricted to the residential sector. The 2020 Pandemic and the impact of rising costs have placed many businesses under increasing financial strain. In fact, the recent collapse of Silicon Valley Bank and Signature Bank are in part attributed to their exposure to the commercial real estate market.

How Do I Know if My Bank is Exposed to Real Estate Risk?

Even if you’re not impacted by the real estate market, you may be inadvertently exposed to real estate risk through your bank. When you deposit money in your bank, you are likely to be completely unaware of what your bank is doing with those funds. So, is your bank investing in higher risk real estate deals?

If you want to find out if your bank is exposed to real estate risk, you will need to perform some research. All banks release financial reports which can provide insight into how they are using their assets. However, there are also some platforms such as MightyDeposits, which can help you to discover where your bank is investing.

For example, Pacific Western Bank has a significant interest in commercial real estate. As of the end of 2022, commercial real estate loans accounted for over 375% of the bank’s capital. Worst still, real estate loans for construction and land, the riskiest sector, amounted to approximately 140% of PacWest’s capital.

However, many banks have now recognized this potential risk and have taken steps to reduce exposure. For example, according to S&P Global Prosperity Bancshares has had the second largest sequential decline in office lending since 2022. The company reduced its office lending 15.1% on the previous year.

Can Banks Fail?

Unfortunately, yes. As we’ve seen recently with Silicon Valley Bank this year and other banks in previous years, in extreme conditions, it is possible for banks to fail. For this reason, it is important to check your FDIC protection and ensure that you are covered.

FDIC insurance is federal insurance that offers protection in the event that a bank or financial institution fails. There are coverage limits, but these are set per depositor, per financial institution. In the slim chance that a bank does suffer a failure, the FDIC insurance will kick in, so you can recover the money held in your account.

Sign Up for

Our Newsletter

Historical Effects of Real Estate Drops on Banks

In the most recent history, the real estate crash of 2007 had a devastating effect on banks. During the crash hundreds of thousands of properties went into foreclosure which triggered the bankruptcy of multiple subprime lenders. At this time, the U.S government had to create a bail out package totalling $236 billion, which was spread across approximately 700 banks.

The market slow down and flat home sale prices created widespread collapses within the mortgage industry including some of the biggest lenders in the U.S such as New Century Financial.

While this has acted as a stark warning for the potential vulnerability of banks, it does highlight that real estate prices can have a massive impact on banks, large and small.

Summary

The economy is an ecosystem with every aspect having an impact on other areas. While it is easy to overlook, real estate prices can be a major factor for banks, increasing risk with rippling effects for homebuyers, savers and mortgage holders.

So, whether you are considering investing in real estate, purchasing a home or simply want to ensure that you’re not at risk, it is well worth performing some research to see what your bank is doing.