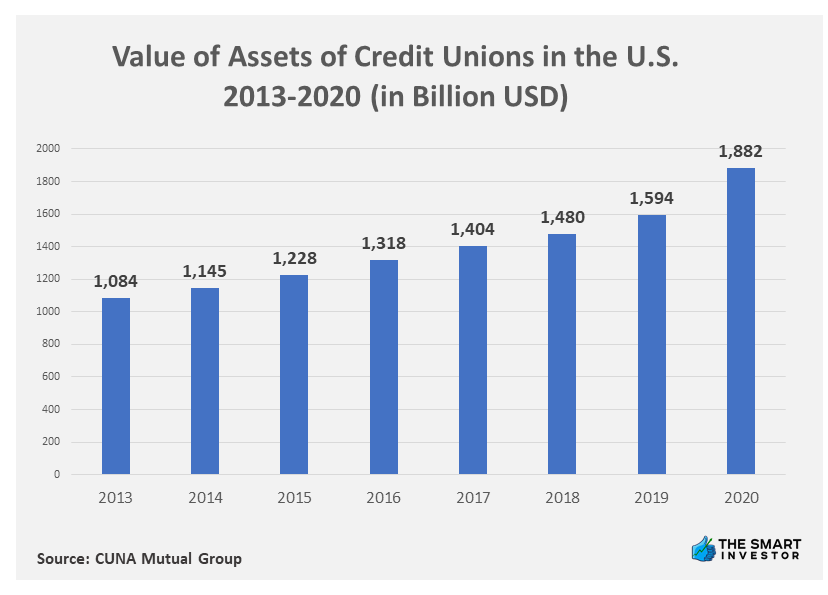

2. Credit Unions

3. Online Money Lenders

Do you want to get a loan without leaving your bedroom? You can get a loan real quick from an online lender – it’s so fast that sometimes, the money is in your account the next business day. However, there are many things to consider before taking such a loan.

Due to the cut-throat competition in the personal loan market, online lenders try so hard to distinguish themselves from traditional lenders. Some of them have innovative lending guidelines that skip the traditional credit-scoring models or offer ‘extras’ like flexible payments, waived fees or schemes to lower interest rate during repayment.

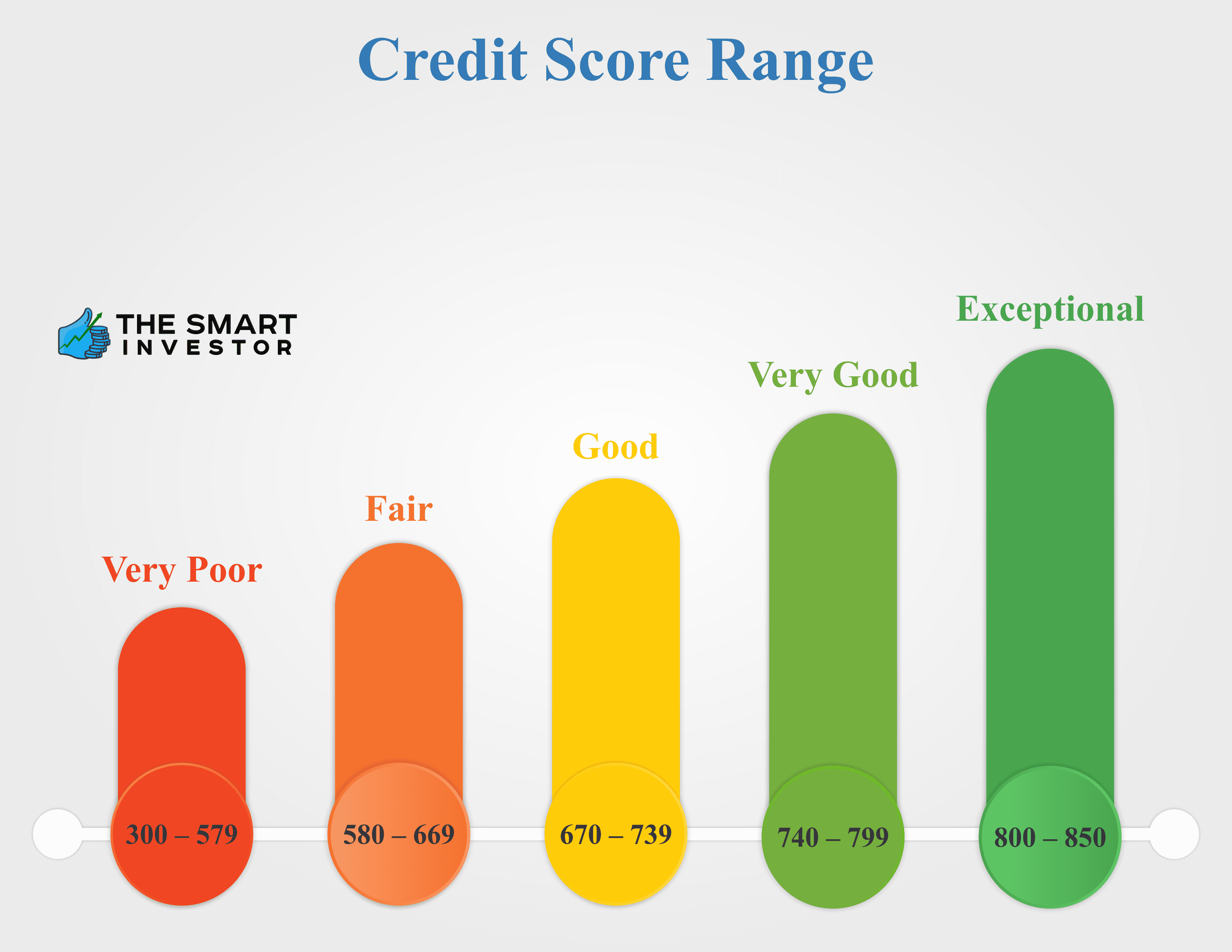

Online lenders like Marcus and SoFi focus on strong-credit borrowers by offering high loan amounts and low-interest rates. They normally consider credit scores of 690 to 719 as ‘good’ while a score of 720 and above is ‘excellent’ (See how your credit score is calculated).

Other lenders try to catch the borrowers with less than perfect credit. Avant and LendingPoint are two of them. Rates will be higher, of course, but it is easier to get an approval if your credit score is just ‘average’ (630 to 689) or ‘bad’ (300 to 629).

What About Bad Credit Borrowers?

Borrowers with bad credit can have these options:

- Find an online lender that caters to borrowers with bad credit. Some of them will factor in non-traditional elements such as earning potential in their decision-making process.

- Get a secured personal loan. In this case, you will need to put up security for your loan such as your car or a certificate of deposit.

- Find a co-signer for your loan. If you have a friend or a relative with good credit, he may help you qualify for a loan or get a lower interest rate. The catch is, your co-signor will have to pay for the loan in case you don’t.

Pros

It’s fast and easy plus there’s not too much paperwork. You just simply key in the information and wait for approval. It’s the best alternative for those with poor credit because these lenders positioned themselves to work with bad or no credit.

Cons

Some of these lenders may charge out-of-this-world interest rates. Do not be surprised if you find that some charge 100% APR – or even more. Once you are caught in, it can be very difficult to break out because the cost of the fee will keep piling up. In many cases, it would be better to first exhaust all other options.

Benefits of a Personal Loan

Yes, they have high-interest rates but personal loans have their own advantages.

- They build your credit portfolio. Personal loans are great in the sense that they can build and expand your credit portfolio within a short span of time. They are also a good way to increase your credit limit since your credit limit is directly dependent on the health of your credit portfolio. You can add to it positively by managing your personal loan properly.

- They are faster to process. Personal loans are quite simple and do not require too many paperwork. Many banks would even grant personal loans instantly for their existing customers with good credit history.

- They are very flexible. Personal loans, by themselves, are flexible enough. Lenders will not restrict you to use the loan amount in a specific way or purpose. You can use it for supporting your business expenses, enjoy a vacation, pay for a wedding, buy something expensive, or renovate your house. This flexibility makes it a popular choice for a number of situations, especially when unexpected items or expenses arise.

Personal Loans: The Impact of Coronavirus

The COVID-19 pandemic in the US has had a devastating impact on millions of Americans. People have lost their jobs, had their hours reduced, or their salaries cut.The pandemic affected most things, regardless of the circumstances.

People will worry about whether they can afford their monthly personal loans due to their changing income. Many lenders are open to working with those who have been forced into difficult financial situations by the pandemic.

You might be eligible to get a payment vacation for personal loans, or to renegotiate monthly payments for a period of time until things return to normal.

Many lenders have increased their requirements for personal loans.Lenders will only give loans to a limited number of people.Other lenders offer personal loans for less than $1,000 to help people get through the pandemic.

Tips to Increase Your Loan Eligibility

If you are looking to boost your eligibility for a personal loan, there a number of changes you can make.

While some will be more difficult than others, it is important to know the key ways your application will be evaluated.

- Boost your credit rating – Your credit rating is a key factor in any type of borrowing. Your credit score will influence the amount you can borrow and how much you pay. Do your best to improve your credit score. Lenders won't deal with anyone who is at high risk of not repaying their obligations.

- Reduce existing debt – Before you apply to a lender, it is important to reduce any existing debt. To show that you have sufficient income to repay your personal loan, the goal is to increase the loan-to–income ratio. Lenders may be concerned if you have multiple forms of debt. They might question your ability to pay your monthly repayments due to other obligations.

- Do not apply for multiple loans at once – When you apply for a personal loan, the lender will raise an inquiry at the credit bureau to assess your risk level. These kinds of difficult inquiries will be a part your credit report. This means that submitting multiple applications to the same lender at once can make you look desperate and could lead to you not being accepted.As they may consider you a greater risk, your chances of being rejected will increase.

- Display all your income – When applying for a job, it is crucial that you show all income sources. Many people have side ventures or money-making endeavors that are important but not part of their main income. This income could help you meet your repayments.This is why you should inform the lender about your income so they can incorporate it into their overall assessment.

- Do not try to get too much – It is crucial that you only view the amount that you need when you apply for a personal loan. Many people will seek to maximize the amount of a personal loan even though they don't need it all. Only apply for the amount you actually need. If you are certain that you can repay the loan in the shortest time possible, don't extend the payback period. If you request a lower amount of funds, lenders will be more inclined to approve your application.

Summary

Personal loans are unsecured fixed-term loans that can serve practically any purpose – pay for your wedding or honeymoon, remodel your home or fly to see the world. Depending on your credit score, a personal loan may even have a lower interest than a credit card – although that is not the general rule.

However, they can still be a safer financial tool because it simplifies paying off your debt through equal installments each month.