Advantages of P2P Lending

Investors are choosing P2P lending as an option because they see that it offers advantages to both borrowers and investors.

Here are some advantages to the borrowers:

- Lower loan interest rates compared with traditional loans from bank credit cards or installment loans.

- Make their transactions in the easy-to-use online interface.

- They are well-informed because of the transparency of the platforms through uniform and clearly disclosed loan terms.

- Borrowers enjoy an efficient decision-making process because of the technology that quickly assesses and assigns risk grades and interest rates to loan applicants.

Here are some advantages to investors:

- Receive high risk-adjusted returns for their money.

- Investors can now invest in a high yield investment class that was traditionally only for institutional investors, for as low as increments of $25.

- Investors can choose and pick the loan to fund because of the transparency and autonomy that the P2P companies provide, as well as monitor loan performance in real-time.

- They have quick access to credit profile data for each loan they approve.

P2P lending platforms have a lower cost than traditional lenders because they maximize the use of technology in their business. In fact, you may look at what they are doing as a form of securitization where, through automation, they divide individual loans of individual borrowers into notes they subsequently issue to numerous investors.

P2P saves a lot of operating costs because they do not have to maintain a physical branch network to service clients and investors. But perhaps the biggest cost saver is that neither the P2P platforms nor the originating banks do not carry the P2P loans on their books. This exempts them from complying to bank capital requirements.

Risks Associated with P2P Lending

Although P2P lending might score appreciable advantages for both investors and borrowers, it is not without imperfections. For one, investors assume more risks than borrowers in a P2P setting. Borrowers can still enjoy the protection that the law provides – including usury laws and regulations against unfair collection practices, misleading advertising, and discriminatory actions. Likewise, since we are talking about lending, P2P investors also open themselves to borrower credit risk, interest rate risk, liquidity risk, and regulatory risk.

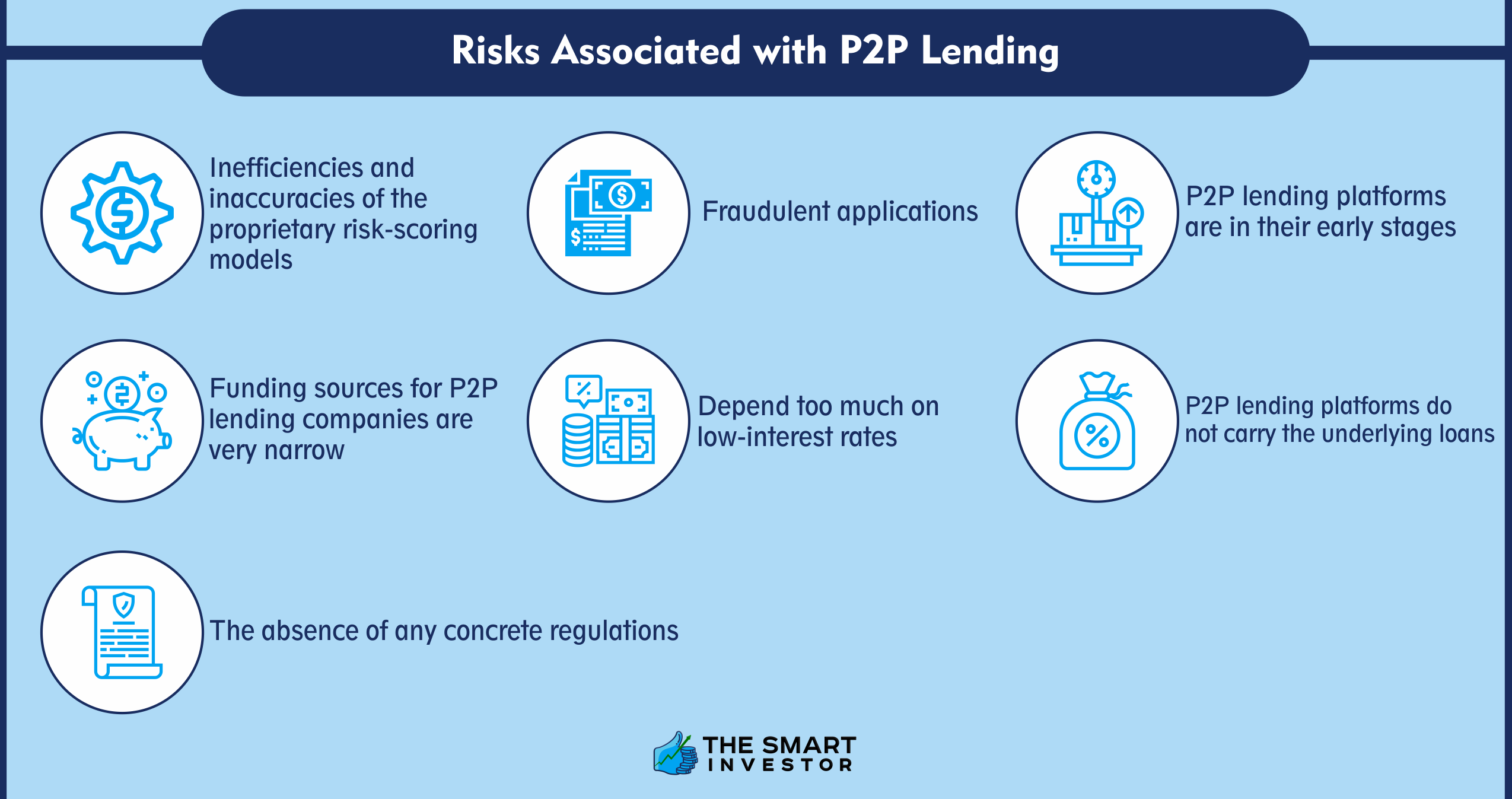

P2P investors can also face the following risks incidental to P2P lending:

- There could be inefficiencies and inaccuracies of the proprietary risk-scoring models of P2P platforms.

- There is a probability of fraudulent applications because of the faceless and paperless process of Internet lending.

- The P2P lending platforms are in their early stages and have a limited operating history.

- The funding sources for P2P lending companies are very narrow, so this limits diversification.

- P2P lending platforms depend too much on low-interest rates to service high transaction volumes.

- P2P lending platforms do not carry the underlying loans they facilitate on their balance sheet, unlike traditional lenders.

- The P2P platforms do not assume any repayment responsibility to their investors if borrowers default on the underlying loans.

- The absence of any concrete regulations to oversee the P2P lending industry (we will discuss this “regulatory purgatory” in more detail below).

Borrower Default Scenario

If you look at their business model, P2P lending platforms make money when they originate and service loans but they assume no risk in case the borrowers default on their loans.

They only pay the investors if the borrowers make a payment on the underlying loans.

Get this: even in case of default and collection, P2P platforms still collect fees.

If a borrower defaults, the P2P platform contracts a collection agency to recover the money. For any amount that the collection agency recovers, the P2P platform will charge a servicing fee, so the respective investors do not get their full share.

However, to mitigate borrower credit risk, P2P lending platforms have taken steps such as providing credit scores for each borrower, offering collection services for errant borrowers, and providing diversification through the purchase of fractional loans.

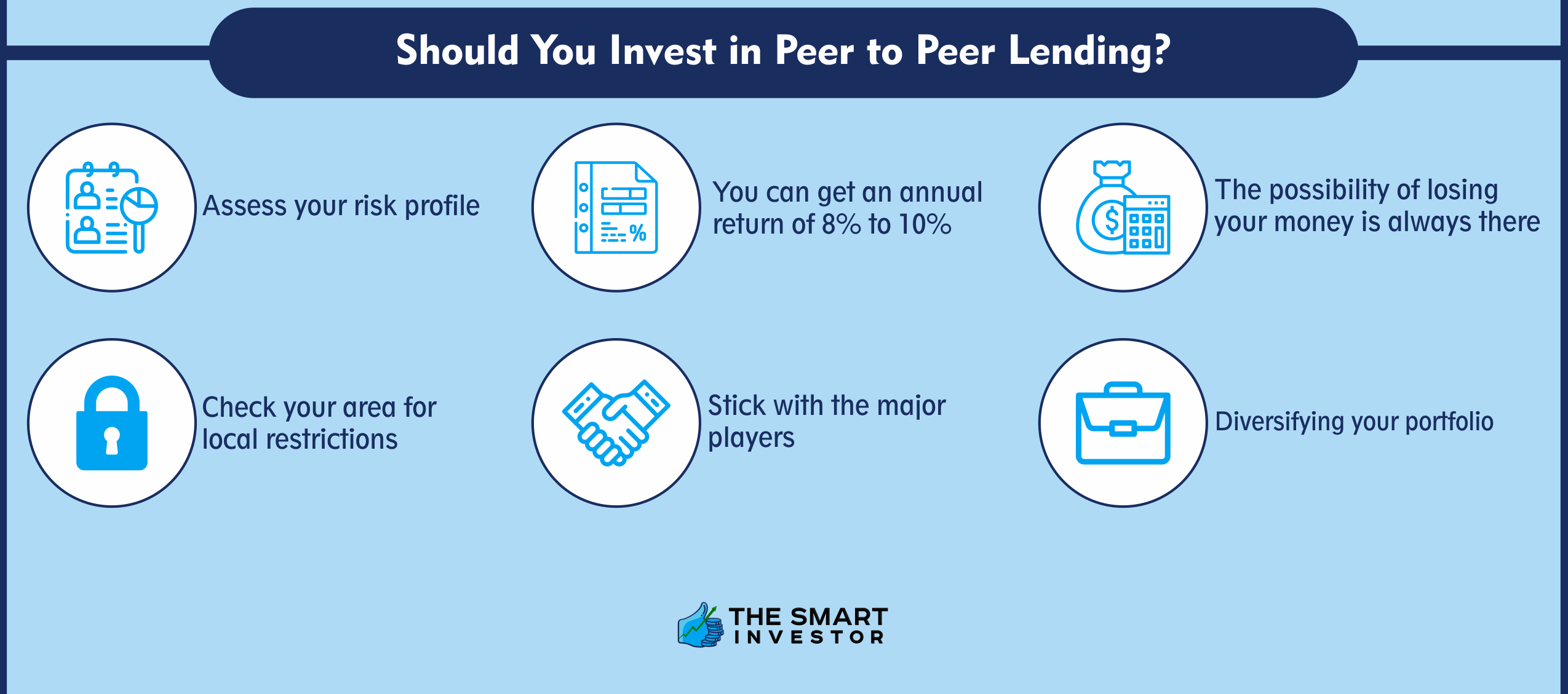

Should You Invest in Peer to Peer Lending?

The first step is to assess your risk profile. Realistically, you can get an annual return of 8% to 10%, but the possibility of losing your money is always there. So, if you can’t afford to lose a big chunk of the principal you will invest, it’s better to skip investing in P2P lending.

Second, check your area if they have local restrictions. For example, certain states like Ohio ban peer-to-peer lending because the state government believes that the risk of loss and outright fraud do not justify the potential benefits.

However, if you really want to venture into peer-to-peer lending, we suggest you stick with the major players who are transparent about their process and have impressive track records. Established groups like LendingClub and Prosper now share the limelight with firms like FundingCircle and Upstart.

They share a registration with the U.S. Securities and Exchange Commission and each one employs sophisticated tools to gauge the risk of potential borrowers. Although those things do not guarantee 100% success for your investment in P2P lending, they can help lessen some of the risks of default.

Lastly, never forget the importance of diversifying your portfolio.

If you want to invest in peer-to-peer lending, just make sure it’s only a part of your portfolio.

And instead of lending $10,000 to one person, consider breaking it up for various borrowers. Ten smaller loans of $1,000 per borrower is a good strategy to spread out your risk and lessen the impact in case one or two borrowers default on their loans.